DeFi, short for decentralized finance, is a system of financial services that runs on public blockchains through smart contracts instead of banks and brokers. Lending, borrowing, trading, earning yield — all of it executes automatically, around the clock, accessible to anyone with an internet connection and a crypto wallet. No forms. No approval process. No intermediary taking a cut.

As of early 2026, the total value locked (TVL) across DeFi protocols sits at approximately $130–140 billion — down from its $178 billion peak in 2021 but representing a battle-tested financial infrastructure with real users, real capital, and growing institutional participation. Ethereum hosts roughly 68% of all DeFi activity.

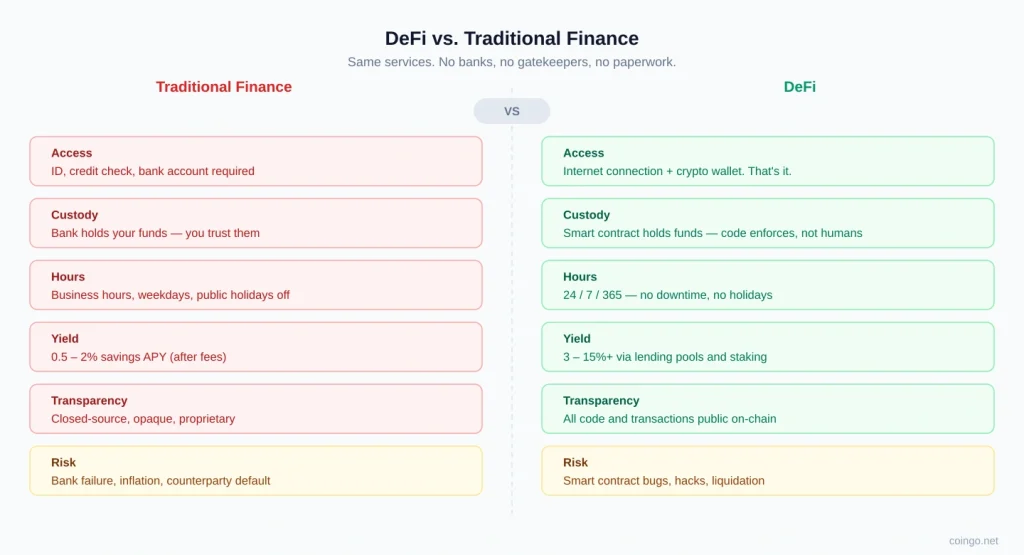

How DeFi Differs From Traditional Finance

The core difference is not which services are offered — both systems handle lending, borrowing, trading, and yield — but who controls the infrastructure. In traditional finance, a bank holds your funds, verifies your identity, and determines whether you qualify. In DeFi, a smart contract holds the funds, the blockchain verifies transactions, and the protocol is open to anyone.

DeFi vs. traditional finance — same services, no gatekeepers

What Are Altcoins? Everything Beyond Bitcoin

How DeFi Actually Works

Every DeFi service runs on smart contracts — self-executing programs deployed on a blockchain. When you deposit funds into a lending protocol, the contract holds them and calculates interest automatically. When you trade on a decentralized exchange (DEX), an Automated Market Maker (AMM) matches your order against a liquidity pool instead of a traditional order book.

Users interact with DeFi directly through a crypto wallet. No account creation, no email, no KYC. The wallet connects to the protocol’s smart contracts, and every transaction is recorded publicly on the blockchain.

“DeFi takes the basic premise of Bitcoin — digital money — and expands it into an entire digital alternative to Wall Street, without the associated costs.”

— Coinbase Learn

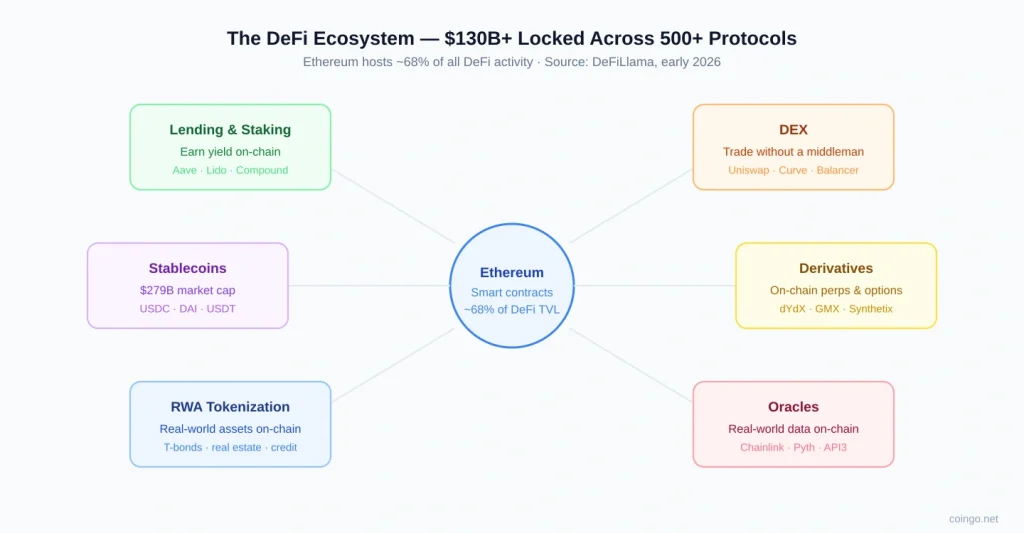

The DeFi Ecosystem: Key Protocols and Categories

DeFi is not a single application — it is an ecosystem of interconnected protocols, each serving a specific role. Lending is the largest category by TVL, led by Aave with over $27 billion and Lido with $27.5 billion in staked assets. Decentralized exchanges like Uniswap process hundreds of billions in monthly volume. Stablecoins — USDC, DAI, USDT — provide the dollar-denominated liquidity that keeps the system running.

| Category | What it does | Key protocols | TVL (early 2026) |

|---|---|---|---|

| Lending & Staking | Earn yield, borrow against crypto collateral | Aave, Lido, Compound | ~$65B |

| DEX | Trade tokens without a centralized intermediary | Uniswap, Curve, Balancer | ~$20B |

| Stablecoins | Price-stable assets for trading, payments, yield | USDC, DAI, USDT | $279B market cap |

| Derivatives | On-chain perpetuals, futures, options | dYdX, GMX, Synthetix | ~$3B |

| RWA tokenization | Real-world assets — bonds, real estate, credit | Ondo, Maple, Centrifuge | Fast-growing |

| Oracles | Feed verified real-world prices to smart contracts | Chainlink, Pyth, API3 | Infrastructure |

Key DeFi categories, protocols and TVL as of early 2026 · Source: DeFiLlama, CoinLaw

The DeFi ecosystem: $130B+ locked across lending, DEXs, stablecoins and more · Source: DeFiLlama

Risks You Need to Understand

DeFi’s openness is also its vulnerability. Because anyone can deploy a smart contract — and because deployed code is immutable — bugs and exploits cause permanent losses. Over $3 billion was drained through DeFi exploits in 2022 alone. Security practices have matured significantly since: audits, bug bounties, and formal verification are now standard in reputable protocols. But risk never disappears entirely.

| Risk | What it means in practice |

|---|---|

| Smart contract bugs | Code vulnerabilities can drain funds instantly — immutable contracts mean no rollback |

| Liquidation | If collateral value drops below threshold, the protocol automatically liquidates your position |

| Impermanent loss | Liquidity providers can lose value relative to simply holding when prices diverge sharply |

| Oracle manipulation | Price feed exploits can distort protocol behavior and enable flash loan attacks |

| Regulatory risk | MiCA (Europe) and GENIUS Act (US) may restrict access or require compliance from protocols |

“Most DeFi protocols must pass through a pragmatic, temporarily centralized incubation phase before they can safely decentralize.”

— Anand Gomes, Paradigm — Consensus Hong Kong 2026

DeFi in 2026: Maturing, Not Slowing

The DeFi market of 2026 is materially more regulated and institutionalized than the yield-farming era of 2020–21. The GENIUS Act in the US and MiCA in Europe have introduced the first coordinated compliance frameworks for stablecoins and DeFi protocols, filtering out weaker projects and signaling that regulators see the sector as permanent rather than experimental.

The most significant growth area is real-world asset (RWA) tokenization — tokenized Treasury bonds, real estate, and corporate credit flowing into DeFi protocols. JPMorgan and Fidelity have begun exploring on-chain lending infrastructure. Yield-bearing stablecoins, whose supply doubled over the past year, are being positioned as a cash alternative for DAOs, corporations, and investment platforms.

For anyone who understands Bitcoin and Ethereum, DeFi is the natural next step: it is where blockchain programmability gets put to work, and where the phrase “be your own bank” becomes operational rather than aspirational.

Sources: DeFiLlama, CoinLaw DeFi Statistics (2026), DL News State of DeFi 2025, Coinbase Learn, CoinDesk, Congress.gov DeFi Overview (March 2026). This article is for educational purposes only and does not constitute financial or investment advice.